Not a change in the physical production model, rather understading how to improve its contribution to society This short introduction is to point out that the recovery of the British economy requires a paradigm shift involving the mechanisms within the economy that operate to generate wellbeing and social harmony. As human endeavour works out more efficient ways of producing products and services, there is a transformative process combining learning by doing accumulating experience associated with the identification of innovations that further refine the utility of output. Associated with the process of innovation and increasing efficiency, it is possible to deliver products and services having used less material and shorter human inputs, involving fewer mistakes and waste and reducing unit costs. This entrepreurial process was that described as the model of how the economy functioned in 1831 by the French economist Jean-Baptiste Say, pictured on the left. It needs to be stated that Say was not an academic economist but in fact had broad involvement in trade and he was a businesman who owned a large spinning factiory in Auchy-lè-Hesdin in the Pas de Calais which employed around 500 people

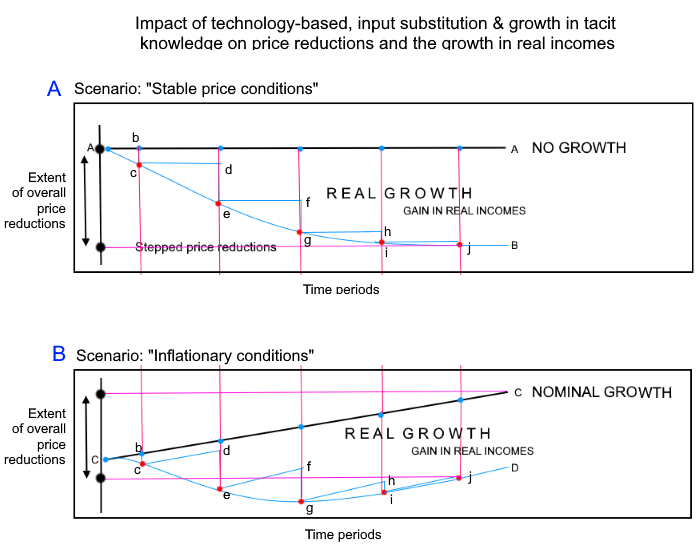

The result of this entrpreneurial process is a capability to reduce unit prices to ensure that they are accessible to the fullest range of incomes of the population so this relative price deflation makes possible a generalised rise in real incomes because more can be purchased for any given disposable income. Because the "cost of living" under such a regime

Such a process is an economic growth path driven by a continual rise in productivity and appropriate price setting. Like the other industrialist, Henry Ford,

The promise of this process is the ability to lower unit prices so that the purchasing power of incomes rises. The Aggregate Demand (AD) paradigm has had poor results

The significance of onshore industry and manufacturing As recounted in the issues page, the larger the industrial and manufacturing sectors the more of the innovation in that sector can bedisseminated to other sectors in the form of more effective, lower cost machines, equipment and devices used in agriculture, mining, other manufacturing activities and services. Since such products are made only in the industrial and manufacturing sectors the source of national economic growth through innovation is generated by the industrial and manufacturing sectors. As the industrial and manufacturing sectors decline in size so does national innovation and derived growth from that sector's impact on the rest of the economy. The impact of post-1975 globalization Between 1975 to 2023 the balance of payments for British industrial and manufactured products rapidly declined causing the country to lose its ability to originate and disseminate its productive innovation and efficiency to the rest of the economy.

Therefore, although businesses investing offshore raised their own profits and justified this in terms on lower prices of imports, the opportunity cost to the nation in terms of the loss of onshore innovation and income for the industrial and manufacturing sectors has had a devastating impact. Basic requirements to recover industry and manufacturing Today, the British economy is largely concerned with logistics of information, financial assets and imported products, constituting a nation of service providers, shop keepers and servants. However, the general capacity of the population and the industrial and manufacturing sector to produce goods that others need in other countries at competitive prices has been drastically diminished. The argument that financial services help to balance poorly performing balance of payments in goods misses the whole point referred to above that the fundamental contribution of industry and manufacturing to innovation in all sectors of the economy and therefore to a self sustained economy has been lost. This is not a new conversation. Nicholas Kaldor, Professor of Economics at Cambridge University, made this point in his inaugural lecture in 1966. In 1975, when UK macroeconomic policy gave more emphasis to monetarism, Kaldor warned that the United Kingdom would end up as we have ended up. Kaldor was fully aware of the imperative of innovation in technology to Britain's future wellbeing having studied the

If I might reduce this issue to a few key points that cause the gaps in the provisions of our economy I would refer to a statement by Henry Ford, "A business that makes nothing but money is a poor business". Financial services, of course, have a role in the economy but cannot be relied upon to create employment with wages that sustain demand at levels for enabling industry and manufacturing to thrive.

This introduction is not a political statement made to denigrate financial services or even the ill-founded AD paradigm. The purpose of this paper is to contribute in the spirit of yet another Henry Ford statements,"Don't find fault, find a remedy; anyone can criticize"." There seems to be a tendency within the economics profession of having grouped themselves into "schools of thought" which tend to be hot houses of peer groups who generate copious volumes of theory and visions that cross reference the work of their peers. As a result, the views of how the economy works, within the economics profession remains confusing and characterized by conjecture. As a systems engineer I find this inability of the profession to not have arrived at a consensus on this matter, extraordinary. Electrical engineers can design circuits of enormous complexity that work, water systems work as do transport systems because those involved in their design and construction have arrived a common understandings on the models they apply along with standard and metrics. Given the serious state of affairs of our economy, it would seem that conjecture, assertion and promotion of visions without an understanding of the mechanisms whereby the economy operates, such as that explained by Say, it is important to concentrate on what will work because what has operated in the past has not been wholly beneficial. Henry Ford again, the man concerned with producing useful products summed this up in this way, "Vision without execution is just hallucination." This might appear to be highly critical of economists, however, I include myself in this struggle we all face for clarity so as to come up with practical solutions to our common predicament. The work I present under the general rubric of the Real Incomes Approach is the result of over 43 years development work but it is not me. It stands by itself subject to analysis and criticism as a basis to improve it or even to abandon it for as yet unidentified by more promising options. Having spent some time on this approach I am confident that our solution does not lie in the domain of the Aggregate Demand paradigm but rather in the territory of the Say model which has a track record of rapid growth and industrial diversification of the economy compared with AD's industrial decline. The Real Incomes Approach is based on the Production, Accessibility & Consumption paradigm, a modification of Say's Economic Treatise sub-heading. A text prepared by the Boolean Library follows has been updated to reflect advances in the state of knowledge of the Real Incomes Approach. This paper is slightly more technical and I therefore ask that anyone wishing clarifications on any part to please send in queries to the forum at: or direct to me at: hector.mcneill@realincomes.org.uk |

1. Given this necessary change in application of the working population which currently does not possess the required skills, what are the implications here for the national educational system from primary through to higher education? |  |

Online course on the Real Incomes Approach to Economics |

| ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| 1. How is the PPR and PPL data collected? | |

| 2. What are the risks involved with respect to any possibilities of creative accounting? | |

| 3. Corporate taxation & accountancy rules are clearly biased against labour. Please explain in more detail how 3P eliminates this issue. | |

| 4. Please explain in more detail the required business rules that will enable managers and labour representatives to take appropriate decisions under 3P. | |

| 5. Please provide more information on the policy provisions with respect to the wage component at the net-PPL stages in each cycle. | |

| 6. Please provide some information on the role of personal taxation under 3P. | |

| 7. Will VAT still apply? | |

A policy-induced process has been returning us to a Dickensian Britain with increasing income disparity & poverty .....  |

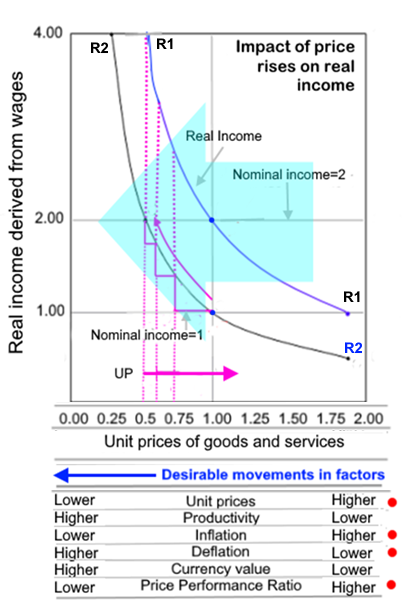

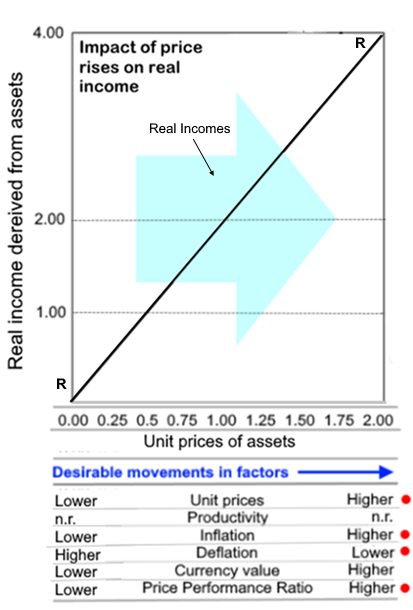

How does policy create income disparity & poverty? One of the questions to be sent to the UK-Independents Forum, questioned the frequent statement in documents issued under the Real Incomes Approach that the Quantity Theory under the Aggregate Demand policy paradigm actually creates income disparity and poverty. This is, of course, a controversial statement, but it is true. The following content is an extract from "Monetary deception", British Strategic Review, Note 11 issued 1st November, 2022. THE INCESSANT RISE IN INCOME DISPARITY THE MARGINALIZATION OF WAGE-EARNERS Income distribution impacts The constitutional impact of financialization Besides intensifying the decline in supply side production, investment and productivity, QE also sustained the decline in real wages. In assessing the impacts of QE, it became evident that this policy greatly benefited one section of the UK constituency made up of asset holders and traders while it prejudiced those working in supply side goods and service provisions in exchange for wages. Not only did QE greatly increase income disparity between these two groups the main reasons for this disparity became more evident. The unit prices of goods and services are an important determinant of the real income or purchasing power of the incomes of all constituents. The purchasing power of the currency is determined by its innate exchange value for goods and services and this is determined by the relative levels and movements in prices. Thus, if prices of goods and services are in general falling the value of the currency rises because more real products and services can be purchased for a given disposable income. If prices of goods and services, in general rise, then the value of the currency falls because fewer real products and services can be purchases for the same disposable income. Therefore, inflation lowers the value of the currency and real incomes and deflation raises the value of the currency and real incomes. Unit prices of goods and services determine “real income”. In Figure 1, the case of wage-earners is shown where price rises (moving from left to right) cause real incomes to decline. Thus, those with a higher nominal income R1R1 see their real income declines as goods and services prices rise. The situation with those on a lower nominal income R2R2 are in a far worse situation. These conditions face all wage-earners under inflationary conditions and wage-earners make up around 95% of the working population and voters. Input to supply side production of goods and services As in the case of wage-earners the relationship of the interests of supply side production sectors is the same in that preference is given to lower input prices which affect production costs. Therefore, the relationship of companies to the prices of their resource inputs and capital equipment and all variable inputs is the same as consumers. Asset holder and asset transaction constituent sources of income On the other hand, the situation for asset holders and traders is shown in Figure 2. In this case, unlike wage-earners, real incomes rise in proportion to prices as indicated by the line ERR. Asset markets are referred to as encapsulated markets in terms of their separation from the volumes of transactions occurring in the production and supply side goods and service markets. These markets also tend to be managed by a smaller proportion of the constituency involving less than 5% of the working population. With large injections of funds, such as experienced under QE, these markets were characterized by rising speculative prices. As a result, the participants in these markets could make significant margins on transactions by simply holding on to the assets for a period of time so that their sales price rose.

As can be readily appreciated the participants in these markets, gain no advantage from falling prices in assets, simply because what they buy is the same as what they sell and the time factor, as opposed to effort, raises the sales price. Therefore, contrary to the state of affairs in goods and services markets the purchasing power of the monetary value of the asset holding is determined by an inverse relationship between assets and innate exchange values. Thus, if prices of assets are in general falling so does the income and wealth of asset holders. If asset prices rise so does the wealth and income of asset holders.

In the case of the inputs to asset trading, these are assets to be eventually sold. Based on the early experience in the New York Mercantile Exchange (NYMEX) starting in the 1970s, this was unlike supply side productive sectors, because input prices of assets have no particular impact on profitability because of the assumption of money injections maintaining a rise in values. Therefore, assets trading as well as asset-based income follow the same straight-line positive relationship with prices. Why are these income lines different? There is an important difference between wage-earners and asset-holders income responses to variations in the prices of goods and services or assets. In the case of income derived from assets the nominal and real incomes rise as a direct proportion to asset prices, therefore the relationship is a straight line. Quite often income paid in the form of bonuses are proportional to the success of individuals making trades which raise the value of assets held and/or sold. As a result, there is no limiting factor on income levels, they are directly proportional to asset prices. In the case of wage-earners, wages tend to be fixed over time so rises in the prices of goods and services take up a curved line relationship because although the nominal income (number of currency units earned) is fixed it also becomes a limiting factor when prices rise. This is why the “cost of living” is a common factor in the political discourse of wage-earners. The real income effects of income sources Therefore, inflation raises the value of assets-based wealth and deflation lowers the value of assets-based wealth. Therefore, the relative benefits of price movements to constituents earning their incomes from asset transactions on the one hand, and the constituents who earn wages for contributing to the production of goods and services, on the other, have an inverse relationship. This also represents very different sets of interests on the part of these constituents on the objectives of macroeconomic policy and the potential impacts on their relative interests, according to the policy instruments applied. There is, therefore, the fact that the real incomes of the majority of the population are safeguarded by policy securing stable or falling price in goods and services. On the other hand, there is a minority of constituents who deal in assets, whose real incomes are safeguarded by policies that facilitate the rising prices of assets. Policy impacts on nominal and real income disparity The British Strategic Review 2022, described how monetarism has had the tendency to drive up asset prices to the benefit of a minority of constituents. On the other hand, monetary policy has no policy instruments to influence wages even although monetarism and financialization has imposed a prolonged period of deficient investment in plant, equipment and training, and wages have tended to be frozen or adjusted infrequently. The leakage of asset prices through into supply side production inputs represent an increasing income from sales and rents to asset-handling constituents while these same transactions cause cost-push inflation resulting in rising unit prices of goods and services . This results in a decline in the real incomes of wage-earners. As a result, the average levels of assets-based income constituents rise at a faster rate than wage-earners whose real incomes often fall. Income disparity, therefore, grows on a continuous basis as a direct function of monetary policy. Constitutional implications of income sources The constitutional implications of the differential impact of different income sources of income on the wellbeing of the constituents are that, as things stand, the results of monetarism over the last 50 years has been one of bias or discrimination against wage-earners. Policy has diminished the relative wellbeing of the majority, while enhancing the wellbeing of a minority. Naturally these circumstances signify that policy has augmented the extent of the differences in the needs of constituents and their demands in relation to economic policies. This impact is clearly at odds with what would normally be considered to be the constitutional objectives of permitting all constituents to pursue their objectives while preventing the pursuit of objectives by any constituent from preventing others pursue theirs. In this case, each group of constituents pursue their objectives but wage-earners face specific constraints imposed, not by asset holders and traders, but as a direct result of policies that place an emphasis on the injection of money into the economy. In the context of universal suffrage, where all people over a specific age have the vote and, in theory, at least, voting leads to a public choice on policies, including economic, the majority of voters should be able to decide on policy matters in their mutual interest to be able to advance the wellbeing of all. |

Introduction For a prolonged period the British government and Bank of England have insisted that rises in wage levels will increase inflation and exacerbate the cost of living. There is an argument that as unemployment falls, labour markets become "tight" so labour is able to demand higher wages and as a result this is why, statistics show that wage settlements are associated with lower unemployment levels. What is less part of this logic is that as inflation rises over time, wage settlements necessarily become higher to compensate for loss of real purchasing power. This short paper examines the main arguments used by the government and Bank of England and reviews the implications with a view to setting out the founding constitutional economic principles to identify an operational framework devoid of such contention. The Phillips Curve

In statistical terms there is a coincidence between the level of unemployment and the levels of wage settlements. In general terms as unemployment falls the level of wage settlements rises.

Although this was the general relationship for the period concerned there was much variance i.e. data points not coinciding with the resultant curve, and since that time this relationship has broken down. The most obvious movement away from this curve occurred after the 1973 OPEC sanctions against petroleum importing countries through rises in petroleum prices in 1973. This gave rise to stagflation or the combination of high general inflation with rising unemployment. Today, we have a similar energy price crisis that also includes natural gas but caused by sanctions imposed by energy importers (USA, EU, UK and some others) on Russia and a refusal to import Russian petrochemicals in a globally tight energy market leading to signifiocant rises in prices. The graph on the right illustrates the break down of the neat Phillips Curve into an indeterminate grey area making any reference to the original Phillips Curve of no particular use to policy decisio-making. People as the shapers of economic principles or as factors of production The whole discussion of economic theory and policy centres on the notion of what is best for people as constituents of the country. In this discussion, and the Phillips Curve is an example, there is the danger of forgetting that people are the reason why we are concerned with economic theory and policy therefore the role of people in the economy is of fundamwental importance in coming to rational conclusions on how policy should be shaped. The discussion surrounding the Phillips Curve is fundamentally about a "factor of production" that seems to have a life of its own because unlike other "factors of production" such as electronic components, steel, coal and commodities, it actually makes demands concerning its price or in this case, income. The reason for this is self-evident, in modern economies income is used tby people to gain access to the basic essentials they require for living, remaining healthy, raise families and remain well-informed to take rational decisions on their own and their children's education and future prospects. Unlike cattle, crates of milk, timber or chemicals people also are constituents who theoretically have the right to vote under the conditions of universal suffrage of one vote for each person in local and general elections. In terms of governance and the identification of appropriate reconomic policies the power of people to select policies proposed should be of significance and operational through the process of public choice. This, one would imagine, should be a reason why labour should not be regarded as simply a factor of production. People's income and freedom of choice as determinants of consumption & aggregate demand As explained in "Back to the Future 1" the income of the population is also the funds used to transact and access those products and services people desire and therefore the population has a dual role both as contributors to production as self-employed or as employees as well as being the consumers of output in conformity with the Say model. Once again this distinguishes labour from all other factor. No major inputs to production contribute to demand; only labour does this. """ Having disussed the PhillipsCurve with fellow students and later with work colleagues it is notable that quite often economists interpret the vertical axis in the Phillips Curve as the general inflation rate. But this is not what the Phillips Curve represents or describes. It only refers to the rise of "prices" in a part of the labour market where settlements are being agreed. orientaion The movement away from the original Phillips Curve is associated with aggregate demand management and a misunderstanding of extreme circumstances . This gives rise to three interpretations:

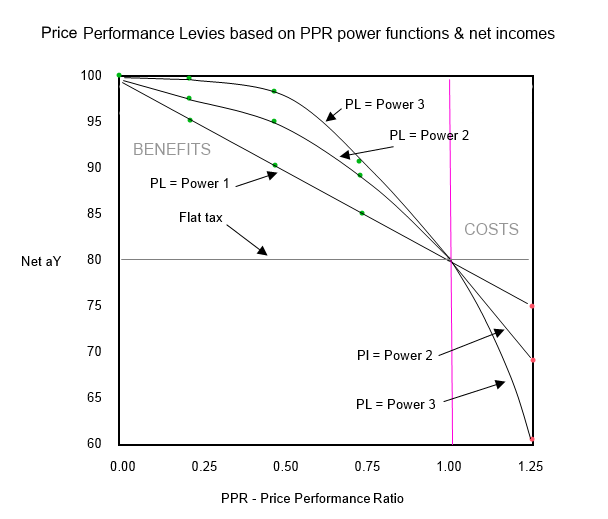

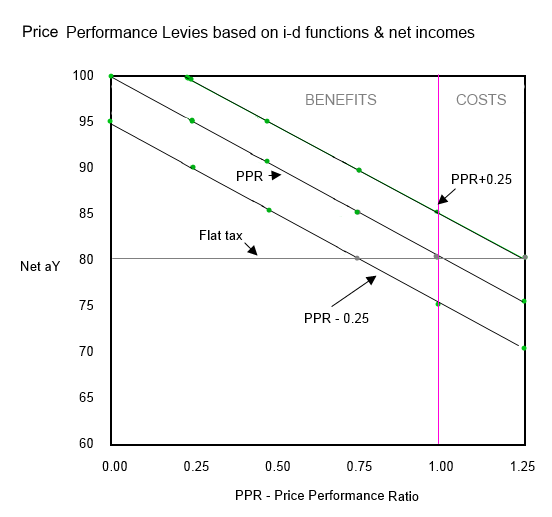

It should be noted that the demand for higher wages is related to nominal incomes compared with changes in prices or income purchasing power. As price rises cause a fall in purchasing power of nominal wages then pressure on wage demands rises. Therefore, there is a direct relationship between inflation, or the cost of living, and wage demands. Thus, wage inflation does not exist in isolation from general price inflation. Based on the Phillips Curve, the impact of Figure 11: Stagflation (rising inflation and the petroleum price increases was unemployment) unexpected because the coordinates of high inflation and rising unemployment moved off the P-C curve to a completely different location. In the absence of adequate productivity gains, high unemployment resulting from high input cost-push inflation and absence of real increases in wages resulted in rising unemployment while maintaining a high level of inflation. Notions of relationships between productivity and the Phillips Curve It is arguable that by raising productivity at a sufficiently high rates and applying these gains to lowering output inflation, the rises in wage rates associated with low unemployment would be lower because the purchasing power of the currency would be higher and therefore the motivation for demanding higher rates of wage rises would be less. In schematic form the original Phillips curve is used to set out different productivity and pricing curves in the diagram on the left. Low productivity with high PPRs would be likely to produce the high wage raises with low unemployment. This is the original P-C curve. A higher level of productivity combined with a lower PPR is likely to result in a lower rate of wage rises with low unemployment as shown by the curve P’-C. The objective of RIP is to encourage a combination of higher productivity with low PPRs and a curve approximating P’’-C so as to contain the levels of inflation at low unemployment. By bringing inflation down to lower levels there is an enhanced probability of these levels of inflation being absorbed by the next phase increases in productivity. This compound graph can be projected in a 3D representation as shown in Figure 13 showing the relationship between inflation, productivity and unemployment. Where productivity is able to lower inflation the aim of Real Incomes Policy is to trade off price productivity against physical productivity which is essential to secure unit costs control. The degrees to which this trade off can be effective depends upon process technologies and the techniques labour forces have learned to deploy. Figure 13: 3D representation of Phillips curves locations and productivity A policy to tackle inflation and sustainable real growth The overall impact of this approach is to slow down the rate of inflation by acting directly on prices. This is a more efficient and effective way to tackling the cost of living crisis than providing consumers with grants and support. This particular approach provides no incentive for companies and manufacturers to moderate prices. However, if their net cash flows depend on their responding to policy and maintaining their cash flows, or increasing them by moderating prices and improving their productivity, then the monies are better spent. The incentive scheme should raise policy traction and the evolution in productivity and innovation should continue. Raising real wages The other principal challenge to macroeconomic management is the question of income distribution and the fact that something like 25% of the working population have wages that are just sufficient to cover essentials but in the lower wage segments support is increasingly required. However, under conditions of inflation this income group faces serious issues in not being able to continue to provide for their essential needs. Whereas Real Incomes Policy aims to moderate and/or reduce unit prices in a counter-inflationary process, this alone, can help raise the purchasing power of people on the low end of wage scales. However, as the title of the policy suggests, the overall objective of policy is to raise real incomes. It is self-evident that if the real incomes of consumers rise so does their purchasing power resulting in increased consumption and throughput of companies rising. If as part of the PPR calculation the productivity gains also involve a marginal rise in wage rates, while securing a low PPR, then the Price Performance Levy payment might be further lowered. This incremental process can end up with the PPR falling well below unity. Thus, the procedure of managing an operational PPR also enables companies to manage the levy they will pay while contributing to the policy objective of raising wages. As a result, such a policy has a long term traction. This is made possible because the whole process remains under the control of the company and workforce decision making rather than arbitrary governmental and policy decisions on interest rates, money injections, government loans and taxation. The whole package is transparent but it needs a sound understanding of consumption schedules of corporate output by product line. This requires an understanding of the price elasticity of consumption of each product to be able to manage this optimally. The Phillips Curve In 1958, Alban W. H. Phillips (1914-1975), published a paper in Economica entitled, "The Relation between Unemployment and the Rate of Change of Money Wage Rates in the United Kingdom, 1861-1957" in which he set out the inverse relationship between money wage changes and unemployment in the British economy, based on the data set for that period. The general relationship which came to be known as the Phillips Curve is shown on the left as P-C. It should be noted that the demand for higher wages is related to nominal incomes compared with changes in prices or income purchasing power. As price rises cause a fall in purchasing power of nominal wages then pressure on wage demands rises. Therefore, there is a direct relationship between inflation, or the cost of living, and wage demands. Thus, wage inflation does not exist in isolation from general price inflation. Based on the Phillips Curve, the impact of the petroleum price increases was unexpected because the coordinates of high inflation and rising unemployment moved off the P-C curve to a completely different location. In the absence of adequate productivity gains, high unemployment resulting from high input cost-push inflation and absence of real increases in wages resulted in rising unemployment while maintaining a high level of inflation. Notions of relationships between productivity and the Phillips Curve It is arguable that by raising productivity at a sufficiently high rates and applying these gains to lowering output inflation, the rises in wage rates associated with low unemployment would be lower because the purchasing power of the currency would be higher and therefore the motivation for demanding higher rates of wage rises would be less. In schematic form the original Phillips curve is used to set out different productivity and pricing curves in the diagram on the left. Low productivity with high PPRs would be likely to produce the high wage raises with low unemployment. This is the original P-C curve. A higher level of productivity combined with a lower PPR is likely to result in a lower rate of wage rises with low unemployment as shown by the curve P’-C. The objective of RIP is to encourage a combination of higher productivity with low PPRs and a curve approximating P’’-C so as to contain the levels of inflation at low unemployment. By bringing inflation down to lower levels there is an enhanced probability of these levels of inflation being absorbed by the next phase increases in productivity. This compound graph can be projected in a 3D representation as shown on the right showing the relationship between inflation, productivity and unemployment. Where productivity is able to lower inflation the aim of Real Incomes Policy is to trade off price productivity against physical productivity which is essential to secure unit costs control. The degrees to which this trade off can be effective depends upon process technologies and the techniques labour forces have learned to deploy . Risk issues for investors The simple introduction of state-of-the-art technologies to a production process using out-dated processes can usually result in predictable quantifiable productivity impacts. This is because quantitative performance data in terms of operational costs and physical productivity of the technology concerned tends to be well-established and classified as good (efficient), average (less efficient) and poor (inefficient) practice. As a result, the risks involved in introducing state-of-the-art technologies are readily apparent and therefore involve more predictable results. Removing the loss from a loss-leader approach The usual investment practice is to carry out such an investment, complete procurement, select the best bid, take delivery and commission equipment and begin production. Usually production proceeds and as efficiency or scales of operation rise unit output prices are established against actual performance in terms of input costs, physical productivity and prevailing market prices. Under RIP companies are encouraged to review in some depth the likely productivity and unit costs projected to some point in the future. Rather than wait for production to reach specific levels before reducing output prices, the technique applied is to anticipate the unit price expected to be feasible at some point in the future. Rather than set this price at the point in time, when it is expected to be feasible, companies establish this price at the time of investment. The effort then goes into managing processes to meet the projected levels of productivity and turnover justifying the price set. This has the effect of reducing the rate of rise in output prices or could even lower unit prices earlier in the process. In terms of constituents this means an earlier real income impact. In both cases, this move provides the company doing this with a competitive advantage vis a vis competing companies. However, his means that the per unit return of output in the initial production stages will be lower or even negative while the output penetrates the market and gains market share. The benefit, from the standpoint of policy is that a degree of control over inflation is secured and consumers have the advantage of being presented with relatively lower rates of price increases, price stability or even falls in unit prices, helping augment their real incomes. The state of affairs for the companies depends upon the markets they serve, consumer income distribution, technologies and inputs deployed and consumption schedules established by the unit price elasticity of consumption. The need to manage the possible In 1981, the author reviewed the RIP concept with Richard Wainwright, then the Liberal Party economics spokesman. He turned out to be one of the few politicians that had taken the time to read and understand the concept presented in a monograph circulated at the time within political party circles as the very first edition of “Charter House Essays in Political Economy”. Wainright was interested in the concepts and his reaction was to state: “If we place this in our manifesto and we win the election we will be faced with the issue of implementing it.” It is certainly the case that at that time, the internet did not exist and the challenge of introducing such a necessary change appeared to be daunting. The oversight of RIP concerning the calculation of PPRs and PPLs would require that all transactions pass through an IT system that sustained an oversight over transactions to avoid “transfer pricing” and a string of possible fraudulent record keeping so as to exaggerate PPR reductions to end up not paying the PPL. These requirements were made evident in 1981 by a senior partner of KPMG the audit company. He considered the proposal to be valid but he pointed out that under the then current regime the necessary information/data for companies to calculate PPRs is not collected by companies. This was an indirect confirmation of Wainright’s position. However, the data is part of corporate transaction records used in accounts. The basic requirements are known. During the last 40 years, the advance in database technologies, security interfaces, improved programming languages and the Internet and modern IT system design techniques, such as Data Reference Modelling, makes the establishment of a standardised system a relatively straightforward issue. Our ongoing costs As matters stand, the costs of continuing as we are, are becoming too high with increasing numbers of people are suffering creating stress and a troubling state of affairs in the country’s social and economic conditions. The constraints established by the current policy-induced debt taxation trap have imposed on government a need to resort to palliative “solutions” that alleviate the suffering of low income constituents, on a temporary basis, but these fail to solve the fundamental problem of the causes of inflation. Having spent time in assessing the political challenges of introducing something like RIP this has given rise to considerations of several options to facilitate its introduction. The potential benefits would appear to be self-evident and growing whereas the costs of introduction of what could be a “game changer” clearly need to be taken into consideration on the political front. Options Below a review of some of the considerations and options available for the introduction of RIP are presented. The advantage of RIP is that is contains a large range of operational options all of which help shift the operational basis for the economy away from the monetarist policy-created debt-taxation trap which has constrained all current government policy propositions to date related to the “solving” the cost of living crisis. Within the Real Incomes development work many options for applying RIP have been developed. They include making the PPL a manufacturing sector run “Development Fund” where payments made remain tagged with the name of the companies paying their PPLs. Rather than build up a fund the operational objective is to attempt to minimise the size of the fund as a reflection of advancing corporate productivity. This collaborative basis set at some distance from government overcomes some of the restrictions under the World Trade Organization which could interpret any government involvement as subsidy and a form of infant industry support. However, a large number of developed nations with now, overbearing service sectors, face the same problem of income disparity becoming higher than in some developing countries. Because the average real incomes have been falling as a direct result of offshore investment largely in developing countries, there has been an effective displacement of former industrial and manufacturing employees in developed nations. This has been associated with a widespread loss of tacit knowledge and capabilities. There is, therefore, a need to base arguments for the essential transitions and expansion of manufacturing on the basis of poverty reduction. It is apparent that as a so-called developed nation, politicians would be reluctant to classify a major change in macroeconomic policy as a poverty reduction measure but conveniently RIP is also a long term growth strategy based on a major investment in innovation, Rather than making RIP a generalized macroeconomic policy it would be better to make it a voluntary scheme within which no corporate taxation would be applied and companies would be allowed to withdraw from the scheme and receive back any accumulated PPL funds on doing so if they are not satisfied with the results. Initial calculations suggest that those joining a RIP scheme would be able to out-compete companies in the same sector who continue under the current policy schemes and taxation regimes. This is not an issue, since it would encourage increasing numbers of companies to transfer to operate under RIP. It is likely that RIP would be better applied to different manufacturing sectors along the lines that operatives within the sector feel would be create the best levels of incentives required to transform the sector. This is because each sector deploys distinct technologies and techniques as well as operating in different input factor and output markets. By making RIP operations sector based there would be a better focus on the specific conditions and technologies of sectors leading to an improved shared knowledge on operational practice and ability to improve the quality of project appraisals. In order to regularize the treatment of labour in a productive fashion so that the PPL operation is linked to PPR estimates that include wage rises, it is probably best to create incentives for the creation of mutual manufacturing operations including the facilitation of any manufacturing company transitioning from plc status to mutual status. This would be reversal of the tendencies encouraged by governments in the 1980s and 1990s of encouraging mutual to become plcs with disastrous results and a steady decline in real wages. This however, would be likely to meet with shareholder resistance except, perhaps in the case of failing companies. Depending upon the levels of impact of RIP the question of personal income tax could come into play with highly successful labour-management operations giving rise to significant controls of inflation, including reduction of unit prices, leading to income tax discounts. One of the most successful roles for government in this system would be to help manufacturing sectors establish detailed and easily accessible information on stat-of-the-art (SoA) technologies combined with adequate economic and financial analyses on potential performance supported by actual survey data on operational best, average and poor practice combined with analyses of the reasons for the differences in performance. It is often the case that practice and performance tends to be linked to operational experience of the workforce and management. The actual difference in performance linked to the learning curve associated with different combinations of technologies and labour need to be collected on a regular basis. This can create data sets that companies can use to estimate the trajectories of their unit costs curves to guide their unit price-setting against likely gains in unit cost reduction. This type of activity needs to be manufacturing sector-based and it might involve teaching and research organizations such as universities. However, this operation should not be slowed up by academic publishing cycles but the raw data should be published regularly and made available to all. Academic institutions should not be permitted to make any claims over the ownership of such data sets which should be a assigned a “Commons” open access categorization. On the other hand, the data should be made readily available engineering and teaching establishments. Concluding Given the dire situation which has been exacerbated by sanctions on Russia, the government is left with little option now other than to provide constituents in need with direct financial support. However, there is an urgent need for the government to act in such a manner as to bring about a change in policies to help the country escape the debilitating debt-tax trap built up by an inappropriate monetary policy dominating macroeconomic management. Post-BREXIT, post-Covid-19 and recovery in a high inflationary environment trending towards stagflation cannot be solved through the manipulation of financial factors based on national accounts and notions of “affordability”. Real Incomes Policy provides an alternative that is a relatively uncomplicated and transparent proposition. It holds the promise of a practical and sustainable approach to help solve Britain’s productivity and real wage crisis. It is not a top-down monolith but contains a range of options on how it might operate, some of which have been outlined. The author: Hector Wetherell McNeill |

Ford

Ford Innovation in a AD world

Innovation in a AD world Pareto

Pareto

The Relation between Unemployment & the Rate of Change

The Relation between Unemployment & the Rate of Change Phillips

Phillips Stagflation and the loss of coherence of the historic

Stagflation and the loss of coherence of the historic